Why Investing Early Is the Key to Achieving Financial Goals

Provided by Rainer Wealth Management

For long-term investors, knowing the difference between what can and cannot be controlled is the key to both financial success and peace of mind. While all investors would like to believe they can predict or even control the direction of the market, experience teaches us that this is difficult to do.

Constructing and managing an appropriate portfolio, while making strategic and tactical allocations based on market opportunities, ideally with the guidance of a trusted advisor, is often the best approach.

However, while following markets and maintaining perspective on the economy is important, an even more fundamental key to success is simply to start saving early, stay invested, and remain focused on long-term financial goals.

What can investors do to benefit from these principles today?

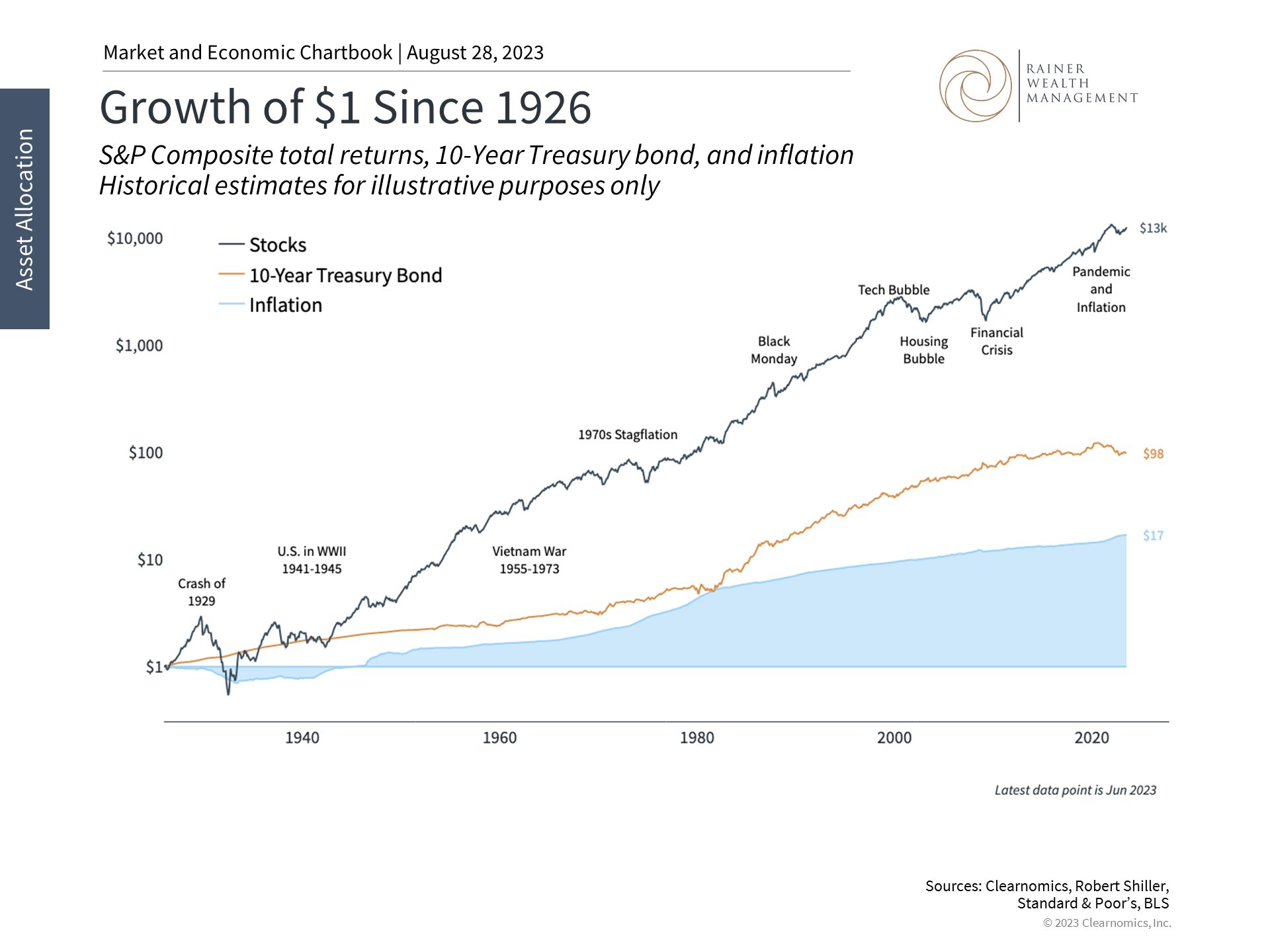

The growth of an initial $1 investment over the last century has been remarkable

Staying financially disciplined has never been more important due to the sheer volume of noise from the media and the financial services industry. It seems as if headlines bounce from one concern to the next every week, with markets constantly swinging from exuberance to distress, as they have already done many times this year. For inexperienced investors and financial professionals alike, this can often be overwhelming.

The reality is that this is nothing new. In 1979, for instance, the cover of BusinessWeek famously proclaimed "the death of equities" due to inflation - just as many did last year. In the short run, these assessments were correct as markets pulled back due to economic shocks and recessions.

However, both the market and economy eventually recovered. Not only has the market experienced strong returns this year, recent volatility notwithstanding, but the past forty years since that magazine cover was published have been some of the best in history.

This pattern plays out when looking back even further: the accompanying chart highlights the growth of $1 invested in 1926 in stocks and government bonds. Amazingly, a $1 stock investment almost a century ago would have grown to over $13,000 today despite the numerous challenges along the way.

Even when invested in risk-free government bonds, the value of that dollar would have climbed to $98. In comparison, inflation has eroded the purchasing power of cash, with $17 now needed to buy what $1 used to.

What this chart shows is that over this time frame, the stock market has created significant wealth for patient investors. However, bonds are also needed to smooth out the bumps along the way in order to preserve wealth.

A proper asset allocation that takes advantage of both asset classes, and possibly many others, is the best way to navigate turbulence while positioning for long run growth. (Please note that this chart uses a "logarithmic scale" to highlight the comparison between stocks, bonds, and inflation. If shown on a linear scale, the steepness of the stock market line would be even more dramatic.)

Saving early can have a significant impact on portfolio values

What's just as important, and fully within an investor's control, is when they begin to save and invest. For example, an initial $1,000 investment, compounded annually at 7%, can hypothetically grow to over $10,000 by age 65 if the investment is made at age 30.

If it's instead made at age 35, only 5 years later, the investment will only grow to about $7,600. The accompanying chart shows this pattern across different ages and return assumptions, highlighting how significant a difference any delay can make.

While investing is often viewed as the activity of following markets, economic data, stocks, and current events, this underscores the fact that budgeting and planning are equally important, if not more so. After all, investors don't get to choose whether they live in an era of low or high annual returns.

However, this chart shows that investing at age 30, instead of age 40, makes as big a difference as experiencing a 5% or 7% annual return over the course of one's life.

The compounding effect of investments requires time

This is because the compounding nature of investments can only work if there is sufficient runway. Given enough time, not only do investment returns add to a portfolio, but those returns generate their own returns, and so on and so forth.

In this way, compound interest is what creates true wealth for investors over long periods of time.

The rule of 72 is a simple way to understand this compounding effect. It is a rule of thumb that estimates how quickly a rate of return would lead to a doubling of a portfolio, or similarly, what return is needed to double a portfolio in a certain amount of time.

For example, with a 5% to 10% annual rate of return - a range consistent with long run historical returns - a portfolio would double in 7 to 14 years. Thus, starting early creates more opportunities to benefit from this effect. Of course, while the rule of 72 is based on pure arithmetic, markets can vary wildly on a week-to-week or month-to-month basis.

The bottom line? While investors should understand and maintain perspective on the market and economic environment, it's equally important to invest early and stay invested through challenging times. History shows that this is the best way to achieve long-term financial goals.

For more information or to schedule a consultation, please give us a call at (925) 217-4280.

Trice C. Rainer, MBA, CFP®

Elizabeth Mintzer, CFP®

390 Diablo Road, Suite 202, Danville, CA 94526

Clearnomics Partnership Disclosure: We have partnered with Clearnomics to create and distribute economic and market commentary. Material presented in economic updates encompass contributions from both Rainer Wealth Management & Clearnomics.

Securities offered through Registered Representatives of Cambridge Investment Research, a broker/dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Cambridge, Protected Investors of America and Rainer Wealth Management are not affiliated. Registered for Securities in CA, IN, MA, MI, NJ, NM, NY, OH, OR, TX, WA.