How Tax Policy Affects the Stock Market

Provided by Rainer Wealth Management

As Benjamin Franklin famously said, “in this world, nothing is certain except death and taxes.” Taxes are no one’s favorite topic but their importance cannot be overstated. Tax policy affects every aspect of our financial lives including how much of our paychecks, investment gains, and dividends we keep, in addition to directing our choices of retirement vehicles, estate planning considerations, and much more. This is why tax planning with the help of a trusted financial advisor is important to best achieve our financial goals.

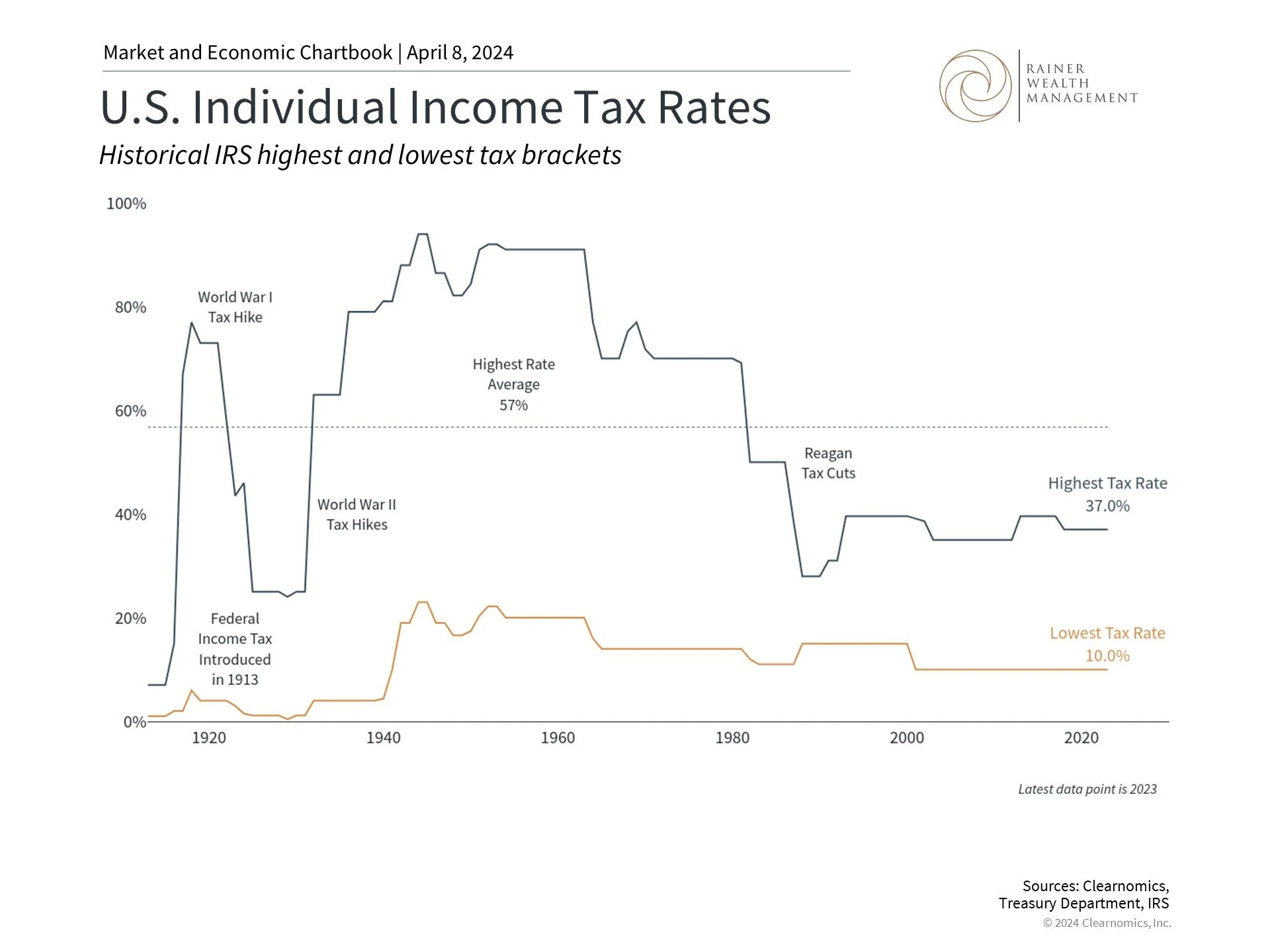

Individual tax rates are historically low

Naturally, some investors also worry about how changes to tax policy will impact the stock market. This is especially true during a presidential election year since the topic of taxes and government spending are politically charged.

What history shows, however, is that while taxes might impact specific industries or asset classes, they have not been the main driver of bull or bear markets. In this context, there are three key facts investors should keep in mind when it comes to their investment decisions.

First, although the history of taxes is complex, it’s fair to say that individual tax rates have been much higher in the past. For instance, the accompanying chart shows that during the 1950s and early 1960s after World War II, the highest rate was a staggering 91%.

The Tax Reduction Act, proposed by President Kennedy and signed into law by President Johnson in 1964, cut federal income taxes by around 20 percentage points across the board, bringing the top marginal rate down to 70%. The bill also reduced the corporate tax rate from 52% to 48%.

Ronald Reagan was then elected in 1980 on a platform of lower taxes and reduced government spending and regulation. Over the course of his two terms in office, the top marginal rate fell from 70% to 28%. This was an era of stagflation and both fiscal and monetary policy sought to stimulate the economy while reigning in supply problems due to high food and oil prices.

Since then, changes to marginal tax rates have been smaller by comparison. The Tax Cuts and Jobs Act signed by President Trump in 2017, for instance, lowered the top individual income tax rate from 39.6% to 37% for households earning more than $600,000, and doubled the amount households can pass tax-free to their heirs.

There have been countless other changes to the tax code including to the number of tax brackets, credits and deductions, how capital gains and dividends are treated, and more. In recent years, inflation adjustments to tax bracket thresholds have also been important to prevent “bracket creep” in which individuals owe more as their incomes are adjusted for rising prices.

When it comes to investing, the most important historical lesson is that the market has performed well in both high and low tax regimes. Most would expect the stock market to perform well during periods of rate cuts. However, the stock market experienced a strong bull market throughout the 1950s and 1960s as the country rebounded from World War II and other global conflicts, when tax rates were near historical peaks.

Economic growth was also generally strong during these decades despite these high marginal rates. Thus, the relationship between the economy, markets and taxes is neither a simple one nor the main driver of growth or market returns.

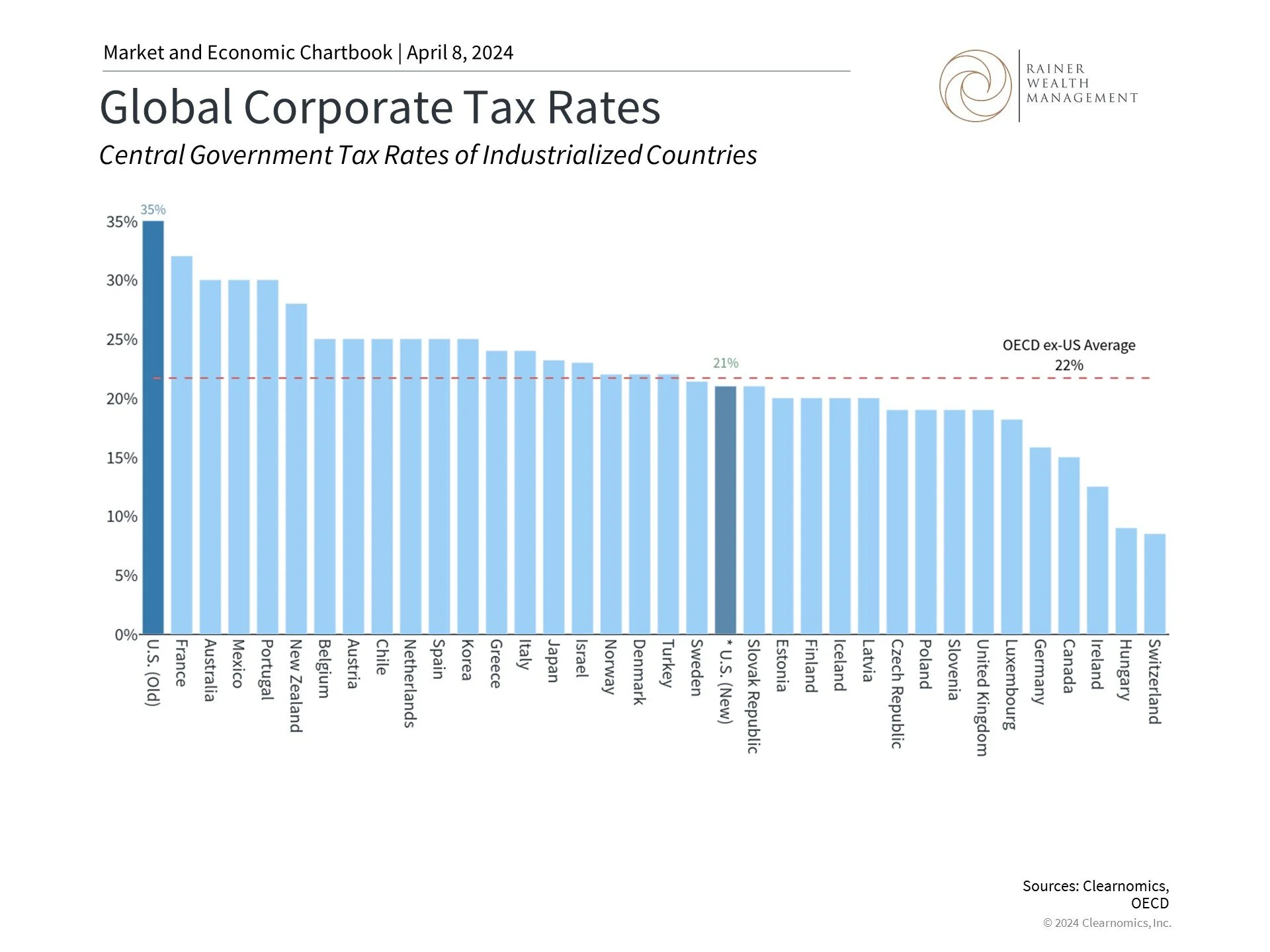

The U.S. corporate tax rates are now more competitive

Second, today’s statutory corporate tax rate is also low compared to historical levels. Prior to 2017, the U.S. had the highest corporate tax rate among OECD countries at 35%, as shown in the accompanying chart. The Tax Cuts and Jobs Act lowered the corporate rate to 21%, placing the U.S. in the lower half of OECD countries.

Of course, the effective tax rate that corporations pay is typically far lower than the statutory rate due to a labyrinth of tax breaks and deductions. Naturally, this is a politically complex topic. On the one hand, corporations are maximizing their tax efficiency based on the existing tax code, which ultimately is good for employees, shareholders, and the overall economy.

On the other hand, this can be viewed as corporations “not paying their fair share,” especially when they are highly profitable, buying back shares and keeping cash overseas. This is one motivation for the 15% Corporate Alternative Minimum Tax (CAMT) for companies with roughly $1 billion in profits included in the 2022 Inflation Reduction Act.

Whether this corporate tax rate remains in effect beyond 2025, along with individual income tax provisions from the 2017 tax cuts, remains to be seen. Regardless, the statutory corporate tax rate has been at this level or higher for the past 85 years during which markets have performed extremely well due to business cycle expansions. Thus, while taxes affect individuals and business owners, it’s important to not overreact when it comes to investment strategies.

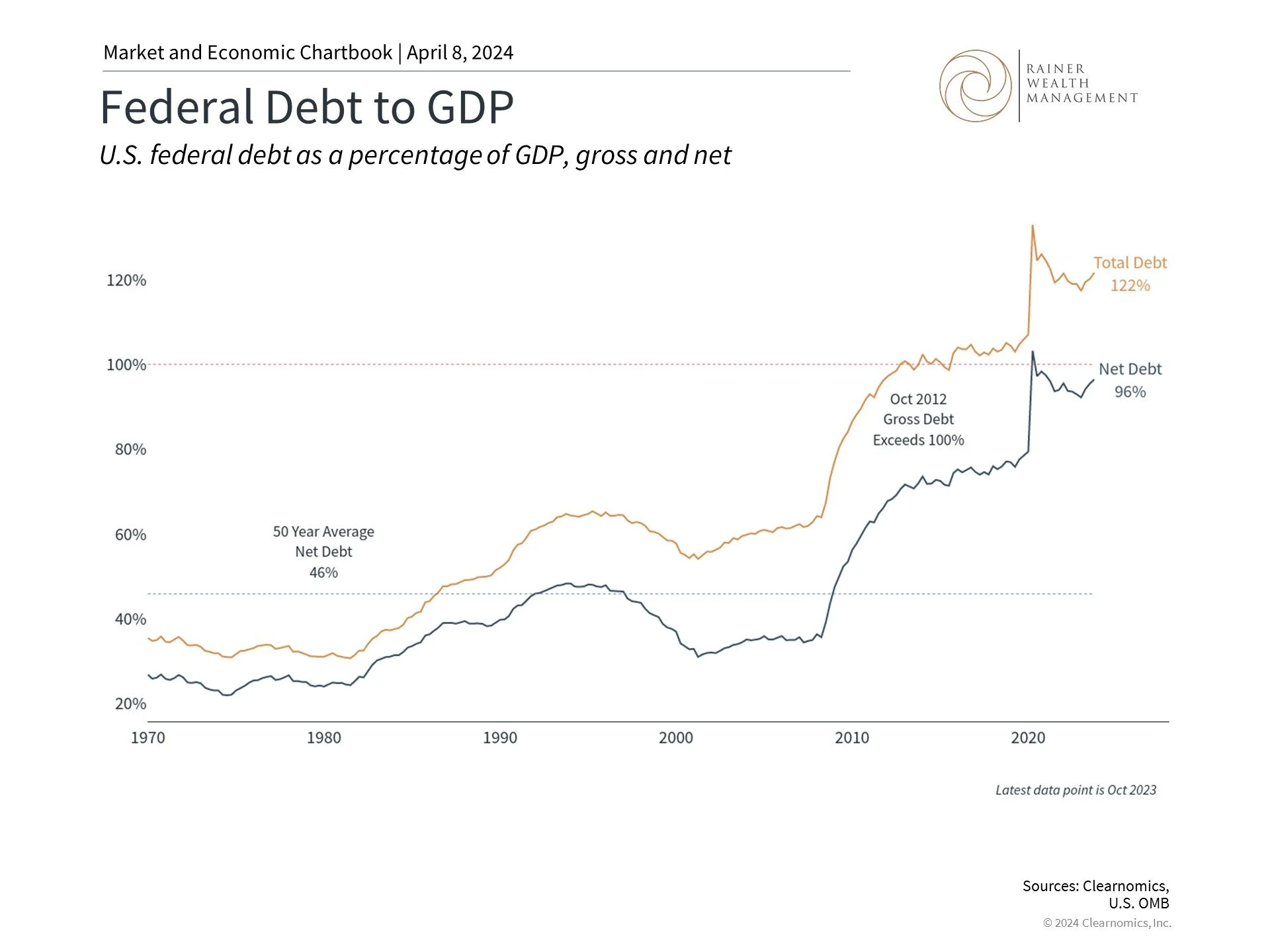

Debt as a percentage of GDP is near historical all-time highs

Third, many investors are worried not only about taxes but also the level of government spending. Today, the federal debt stands at $33 trillion, more than 10 times its 2000 levels, representing over 120% of the country's gross domestic product. Even when adjusting for what the government owes itself, resulting in what is known as "net debt," this number has risen to 96% of GDP.

As the accompanying chart shows, the debt has ballooned during periods of economic crisis when the government spends to stimulate the economy, such as during the 2008 financial crisis and the recent pandemic.

There are only two ways to improve budget deficits: reduce spending and/or increase revenues. Reducing spending, especially non-discretionary items such as Social Security and Medicare, have been nonstarters in Washington. Additionally, the government has not run a balanced budget since the Clinton and Nixon administrations, at the turn of the century and in the early 1970s, respectively.

Thus, some investors worry that taxes could increase in the coming years. While how and when this could occur is still uncertain, it is clear that today’s tax rates are relatively low by historical standards. It’s important for all investors to consider current tax policies while planning for the future with the help of a trusted advisor.

The bottom line? Taxes are low by historical standards and markets have performed well across both high and low tax periods. Investors should maintain perspective and not overreact to tax policy changes when it comes to their investment plans.

For more information or to schedule a consultation, please give us a call at (925) 217-4280.

Trice C. Rainer, MBA, CFP®

Elizabeth Mintzer, CFP®

390 Diablo Road, Suite 202, Danville, CA 94526

Clearnomics Partnership Disclosure: We have partnered with Clearnomics to create and distribute economic and market commentary. Material presented in economic updates encompass contributions from both Rainer Wealth Management & Clearnomics.

Securities offered through Registered Representatives of Cambridge Investment Research, a broker/dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Cambridge, Protected Investors of America and Rainer Wealth Management are not affiliated. Registered for Securities in CA, OH, TX, WA.