What the Fed’s Outlook Means for the Bond Market

Provided by Rainer Wealth Management

The path of interest rates has been highly uncertain over the past few years due to inflation, economic growth, and the Fed. The 10-year U.S. Treasury yield, for instance, jumped from 3.8% at the end of last year to a high of 4.7% in April, before settling around 4.2% more recently.

Higher rates have defied the expectations of investors and economists, creating a challenging environment for the bond market, since rising rates push down bond prices. However, with inflation beginning to improve, many finally expect the Fed to begin cutting rates by the end of the year. What perspective do diversified investors need to stay balanced in the months ahead?

Improving inflation is supporting the bond market

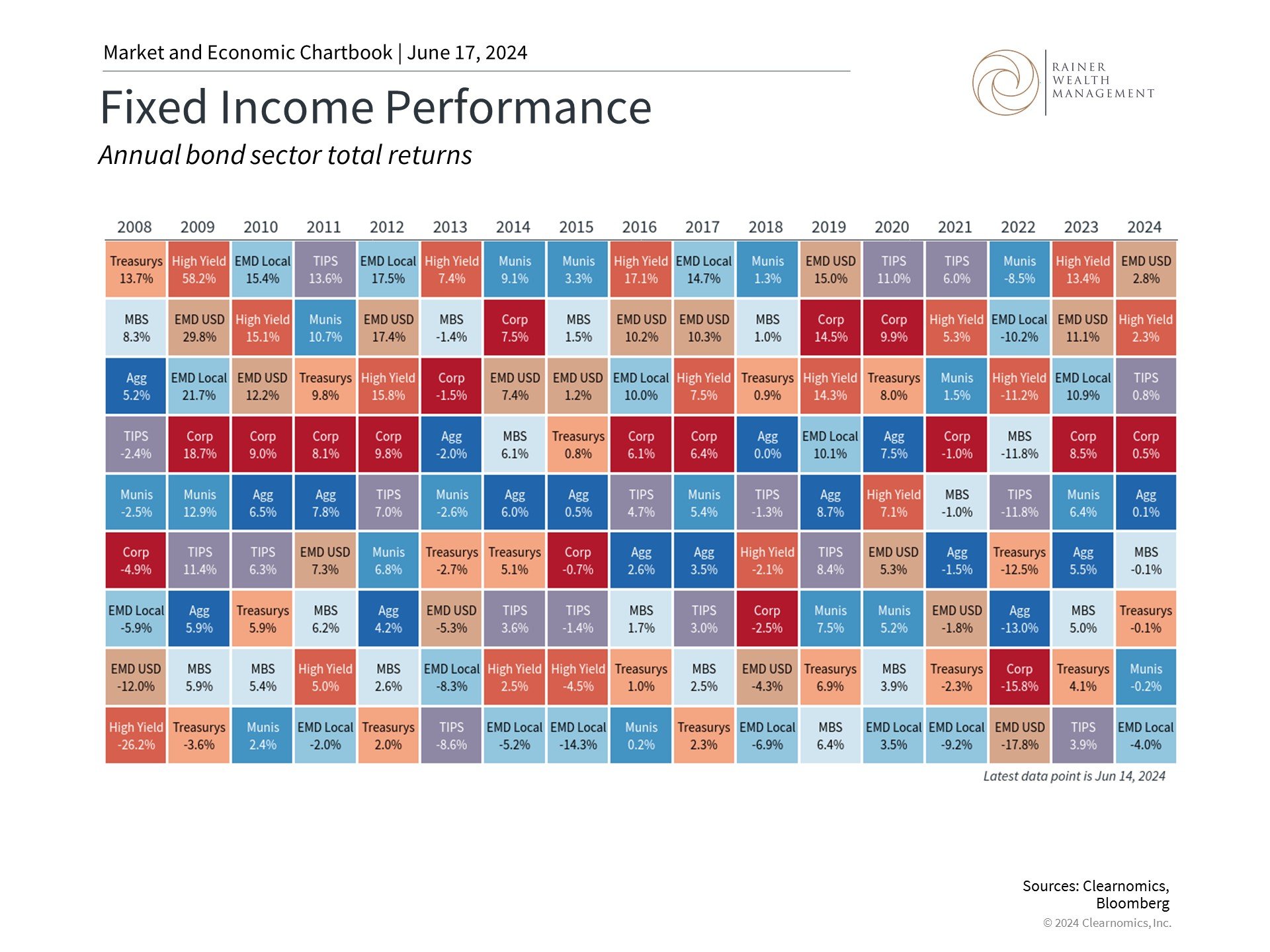

This chart shows sector total returns sorted from best to worst each year. Fixed income sectors included are Bloomberg U.S. Aggregate Bond Index, Bloomberg EM USD Aggregate Index, Bloomberg U.S. Corporate High Yield Index, Bloomberg Municipal Bond Index, Bloomberg U.S. Treasury Inflation Notes Index, Bloomberg U.S. Corporate Index, Bloomberg U.S. Treasury Index, Bloomberg U.S. Treasury, Bloomberg U.S. Mortgage Backed Securities Index, and Bloomberg EM Local Currency Government Index.

Recent economic reports suggest that inflation could finally be improving. After hotter-than-expected readings in the first quarter of the year, the latest Consumer Price Index data showed no change in overall prices in May for the first time in almost two years.

Core CPI rose 0.2% in May, or 3.4% year-over-year, a healthy deceleration from the previous month’s 3.6% pace. Housing costs remain stubbornly high but removing them from the picture results in core inflation of only 1.9% over the past twelve months. Other data, such as the Producer Price Index, have shown signs of deflation after also coming in higher than expected in previous months.

These developments, along with new Fed guidance, have pushed rates lower in recent days, supporting bond prices. The Bloomberg U.S. Aggregate Bond Index, a measure of the overall bond market, is now flat on the year after declining as much as 4% in April. Investment grade and high yield bonds are now positive on the year as well. This is in sharp contrast to 2022 when bonds fell into a bear market during the historic jump in interest rates, before stabilizing and rebounding in 2023.

As interest rates fall, bond prices tend to rise since the yields on existing bonds become more attractive. The yield on the investment grade bond index, for instance, is hovering around 5.3% - well above the average of 3.7% over the past 15 years. High yield and mortgage-backed securities are generating 7.9% and 5.1%, respectively.

It's difficult to overstate the importance of these yield levels. For much of the decade after the 2008 financial crisis, many investors wondered if yields would ever improve as policy rates remained near zero – or even negative in some parts of the world.

Those who rely on their portfolios for income were forced to “reach for yield” – i.e., to take on more risk to generate sufficient income such as by buying riskier bonds or replacing them with dividend-paying stocks. Today, although price volatility has been elevated, retirees and investors with long time horizons can finally benefit from the most attractive yields in years.

The Fed is still expected to cut rates later this year

This chart tracks the Federal Funds Rate lower limit. The dotted lines indicate the Federal Open Market Committee's (FOMC) participants' median assessments of appropriate path for the Federal Funds Rate, based on the Summary of Economic Projections.

While performance numbers are always subject to change, they reflect the possibility of both rate cuts later this year and settling inflation rates. This is important because the market’s expectations for Fed rate cuts have been all over the map this year, causing longer-term rates to fluctuate as well.

In January, fed funds futures were implying that the Fed would have to cut several times due to a possible recession. When the economy stayed strong and inflation remained stubborn, expectations flipped.

Inflation rates are still higher than the Fed would like, but recent improvements are exactly what policymakers want to see. Higher policy rates, after all, are meant to tighten economic activity, slow spending, and keep inflation in check. In their latest statement following the CPI report, the Fed stated that “there has been modest further progress toward the Committee’s 2 percent inflation objective.”

At his press conference, Fed Chair Jerome Powell also emphasized that the Fed is sensitive to the “two-sided risks” of keeping the fed funds rate higher for longer. Specifically, high policy rates may combat inflation, but they could also slow the economy in undesirable ways. Last year’s banking crisis, for instance, was due in part to the impact of rising rates on some banks that were exposed to rate-sensitive long-term bonds, commercial real estate, cryptocurrencies, and more.

The Fed’s latest projections call for one rate cut later this year, revised down from three, with the remaining two cuts pushed into next year. While this reflects the Fed’s sense of caution, it should also be taken with a grain of salt since these forecasts are often revised. Timing was partly an issue since the latest positive CPI data were released just hours before the Fed’s announcement. Market-based measures still suggest that two rate cuts are possible this year with the first occurring in September or November.

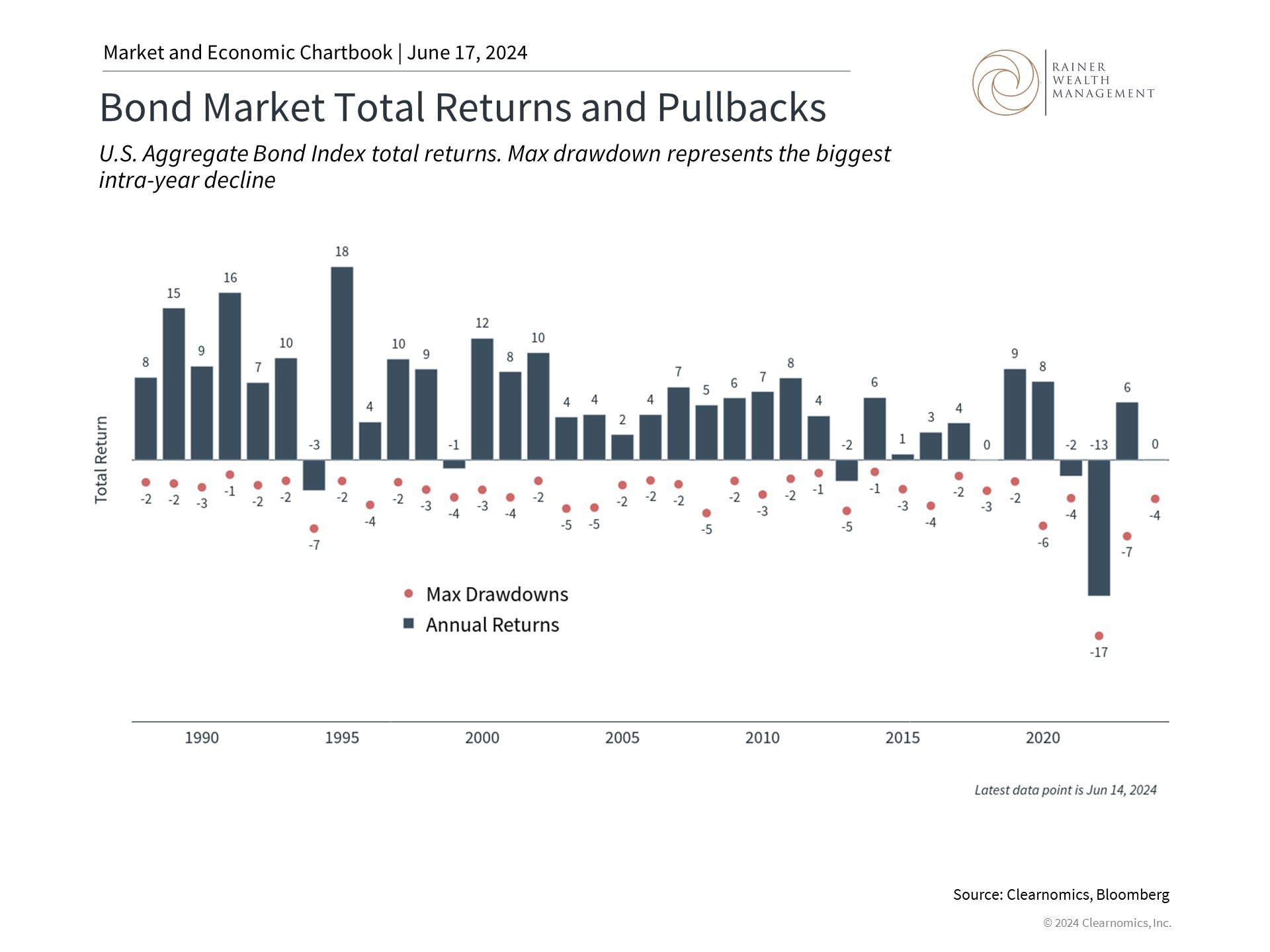

Bonds can still provide portfolio balance

This chart shows the annual returns and largest intra-year decline for the Bloomberg U.S. Aggregate Index using total returns. The largest intra-year decline is measured as the largest peak-to-trough decline during the calendar year.

If rates do finally ease, the historical role of bonds as portfolio diversifiers could receive a boost. Traditionally, bonds have helped to balance portfolios since they tend to move in the opposite direction of stocks. For instance, when the economy and stock market stumble, interest rates tend to fall which supports bond prices.

This pattern was amplified beginning in the mid-1980s as steadily declining interest rates led to higher bond prices over the subsequent 40 years. This allowed both stocks and bonds to experience a strong bull market, with bond prices holding steady and rising even more during periods of stock market turmoil. 2022 saw a reversal of these trends with both asset classes falling due to unexpected inflation. These dynamics called into question the traditional role of bonds as portfolio stabilizers and consistent sources of yield and returns.

What does the future hold for the relationship between stocks and bonds? If inflation does improve and the Fed is able to cut rates, then traditional patterns could finally reemerge. The chart above highlights the historical pattern for bond returns. Inflation scares and monetary tightenings such as in 1994, 1999 and 2013 can result in poor bond returns. However, once these episodes pass, investors have tended to return to bonds as important sources of yield and portfolio diversification.

Although the last two years have been challenging for diversified investors, the possibility of more stable rates means that bonds could be increasingly attractive. In the meantime, it’s important to stay diversified across asset classes as the Fed nears its first rate cut and the price pressures across the economy continue to subside.

The bottom line? Bonds continue to be an important part of any diversified portfolio. While the outlook remains uncertain, improving inflation and the possibility of Fed rate cuts could be positive for the bond market in the months ahead.

For more information or to schedule a consultation, please give us a call at (925) 217-4280.

Trice C. Rainer, MBA, CFP®

Elizabeth Mintzer, CFP®

390 Diablo Road, Suite 202, Danville, CA 94526

Clearnomics Partnership Disclosure: We have partnered with Clearnomics to create and distribute economic and market commentary. Material presented in economic updates encompass contributions from both Rainer Wealth Management & Clearnomics.

Securities offered through Registered Representatives of Cambridge Investment Research, a broker/dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Cambridge, Protected Investors of America and Rainer Wealth Management are not affiliated. Registered for Securities in CA, OH, TX, WA.